Defined Contribution Health Plans

Filed under: Health Care ReformUnder a defined contribution health plan, an employer gives its employees a fixed contribution to purchase health insurance coverage. Employees use that money to buy or help pay for a health insurance plan they select for themselves. The concept of a defined contribution employee benefit is not new; most employees are familiar with the defined contribution approach through their retirement benefits. However, recently there has been an increased interest in the defined contribution approach to health benefits.

The heightened interest in defined contribution health plans is mainly due to the increasing costs of health coverage and changes made by the health care reform law, or the Affordable Care Act (ACA). Also, in addition to the public health insurance Exchanges mandated by ACA in 2014, private exchanges have emerged as marketplaces for employees to select a health plan from an array of available options.

Because defined contribution health plans are a relatively new trend, it is not yet clear whether employees will find this arrangement acceptable and whether it will be a competitive advantage or disadvantage in the employer's labor market.

OVERVIEW OF DEFINED CONTRIBUTION APPROACH

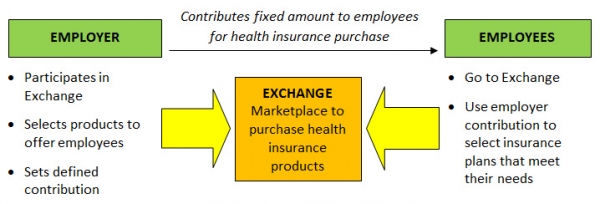

The following is a conceptual overview of the defined contribution health plan model:

The defined contribution approach gives employees more choice and responsibility when choosing health coverage. It also allows the employer to limit its financial contribution for employees' health coverage to a fixed amount, which moves the risk of premium increases to its employees. However, some employees may be skeptical about the defined contribution approach and may prefer the traditional model of health coverage. This could put an employer at a disadvantage in the marketplace if its competitors continue to offer traditional health coverage for their employees.

EMPLOYER CONTRIBUTIONS

HRAs

To maximize tax savings under a defined contribution health plan, employers have typically established health reimbursement accounts (HRAs) for making their contributions. Unlike health flexible spending accounts (FSAs) and health savings accounts (HSAs), HRAs can be used to reimburse health insurance premiums. Also, unlike an HSA, an individual does not need to be covered under a high-deductible health plan (HDHP) to participate in an HRA. This has made HRAs particularly compatible with defined contribution health plans.

Effective for 2014, ACA prohibits all annual limits on essential health benefits. Whether an HRA will be permitted under ACA's annual limit rules mainly depends on whether the HRA is an "integrated HRA" or a "stand-alone HRA." Employers using HRAs in connection with their defined contribution health plans should examine their HRAs to make sure they are compliant for 2014.

Integrated HRAs

An HRA integrated with other group health coverage is not required to satisfy ACA's annual limit restrictions if the other coverage alone satisfies the annual limit restrictions. An HRA is considered integrated with an employer's group health coverage if, under the terms of the HRA, the HRA is available only to employees who are covered by employer-sponsored coverage that meets ACA's annual limit requirements.

A set of frequently asked questions (FAQs) from January 2013 addresses when an HRA is considered "integrated" with other coverage. In the FAQs, the federal agencies in charge of implementing ACA state that they intend to issue the following future guidance on HRAs:

- An employer-sponsored HRA cannot be integrated with individual market coverage or with an employer plan that provides coverage through individual policies.

- An employer-sponsored HRA may be treated as integrated with other coverage only if the employee receiving the HRA is actually enrolled in that coverage.

Stand-alone HRAs

Some stand-alone HRAs are not subject to ACA's annual limit restrictions because they fall under an exception, such as retiree-only HRAs, vision-only or dental-only HRAs and certain HRAs that qualify as health FSAs. However, beginning in 2014, stand-alone HRAs that do not fall under an exception will not be permitted due to ACA's prohibition on annual limits. This generally means that employers will not be able to offer a stand-alone HRA for employees to purchase individual coverage, inside or outside of an Exchange.

However, the FAQ guidance gives stand-alone HRAs more time to comply with the annual limit restrictions with respect to amounts credited before 2014.

Cafeteria Plans

Another way for employers to maximize tax savings is to make their employee health insurance contributions through a Section 125 Plan, or a cafeteria plan. Employers can offer the employees "credits," or employer money, under a cafeteria plan that can be used to purchase qualified benefits, such as major medical insurance.

Under ACA, individual health coverage offered through an Exchange generally will not constitute a qualified benefit that can be purchased on a pre-tax basis through a cafeteria plan. However, Exchange coverage may be funded through a cafeteria plan if the employee's employer is eligible to participate in the Exchange and elects to make group coverage available.

MARKETPLACES FOR COVERAGE

Public Exchanges

Effective Jan. 1, 2014, ACA requires each state to have an Exchange to provide a competitive marketplace where individuals and small businesses will be able to purchase affordable private health insurance coverage. The Department of Health and Human Services (HHS) will operate a federally facilitated Exchange (FFE) in any state that does not establish its own Exchange.

Individuals and small employers with up to 100 employees will be eligible to participate in the Exchanges. However, states may limit employers' participation in the Exchanges to businesses with up to 50 employees until 2016. Beginning in 2017, states may allow businesses with more than 100 employees to participate in the Exchanges. Enrollment in the Exchanges is expected to begin on Oct. 1, 2013.

Each ACA Exchange will have Small Business Health Options Program (SHOP) to assist eligible small employers to provide health insurance for their employees. A SHOP must allow employers the option to offer employees all qualified health plans (QHPs) at a level of coverage selected by the employer—bronze, silver, gold or platinum. In addition, SHOPs may allow an eligible employer to choose one QHP for its employees.

On March 11, 2013, HHS issued a proposed rule that would delay implementation of the employee-choice model as a requirement for all SHOPs until 2015. For 2014, the FFE's SHOP would not allow eligible employers to offer their employees a choice of QHPs at a single level of coverage and would assist employers in choosing a single QHP to offer to their employees. Under the proposed guidance, the employee-choice SHOP model would be optional for state-based Exchanges for 2014.

Private Exchanges

Private health insurance exchanges are emerging as an alternative to ACA's public Exchanges. When using a private exchange, employers contract with the exchange, set a defined contribution and select the health insurance products to be offered to employees. Employees then go to the exchange's online marketplace and, using the employer contribution, select a plan from the available options.

Private exchanges can provide more flexibility than ACA's Exchanges.

- Private exchanges can offer a broader range of insurance products, such as life insurance, and their products can be tailored for different employer segments.

- Although ACA prohibits large employers from using the Exchanges until at least 2017, there is no similar restriction for private exchanges. Thus, small and large employers can use private exchanges to provide group health insurance benefits to their employees.

- Private exchanges are currently operating to provide employees with a choice of health insurance products, while the SHOP's employee choice model will likely be delayed until 2015.

Private health insurance exchanges are a relatively new model for providing group health insurance benefits. The availability and success of private exchanges most likely depends on employers' willingness to move from a traditional health plan to a defined contribution health plan.

This article is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel for legal advice.

Design © 2013 Zywave, Inc. All rights reserved.

The Loop Archives

- Healthcare Reform Update

- Concierge Medicine: The Answer to the “Patient Mill”?

- Pay or Play Penalty – Affordability Safe Harbors

- ACA Mandates — Different Measures of Affordability

- Q&As on Medical Loss Ratio Rules

- Medical Loss Ratio Rules

- White House Announces Transition Policy for Canceled Health Plans

- Taxes and Fees under the Affordable Care Act

- Health FSAs — Changes for 2014

- Health Insurance Exchanges: Multi-state Plans

- Health Reimbursement Arrangements (HRAs) — Changes for 2014

- Reinsurance Fees — Possible Exemption for Certain Self-insured Plans

- Final Rule Issued on Exchanges, Premium Stabilization Programs and Market Standards

- New Exemption from the Individual Mandate for Exchange Enrollees

- Insurance Marketing Nondiscrimination Reforms for 2014

- Health Care Reform Fees – Special Rules for HRAs

- FAQs on the Use of Exchanges for Ancillary Insurance Products

- Employer Penalties – Multi-employer Plans

- Transition Relief for Expatriate Health Plans

- Small Business Health Options Program (SHOP) and Multi-state Plans

- Health Care Reform – The Individual Mandate

- Model COBRA Election Notice Updated for ACA Changes

- Final Rules on Workplace Wellness Programs

- Effect on HRA Contributions and Wellness Program Incentives on Affordability

- Rating Restrictions for Health Insurance Premiums

- Pediatric Dental Care Coverage

- Defined Contribution Health Plans

- Exchange Eligibility Rules for Medicare Beneficiaries

- Deal to End the Government Shutdown and its Impact on Health Care Reform

- Small Employer Health Care Tax Credit: Changes for 2014

- Limits on Out-of-Pocket Maximums: Full Compliance Delayed for Some Health Plans

- FAQ on Exchange Notice Penalties

- Proposed Rules Released on Reporting for Issuers and Self-funded Employers

- IRS Issues Final Rules on Individual Mandate Penalties

- Agencies Release Guidance on HRAs, Health FSAs and Cafeteria Plans

- The Basic Health Program (BHP)

- HHS Announces Delay of Certain FF-SHOP Functions

- Impact of the Government Shutdown on Health Care Reform

- Verification of Eligibility for Exchange Coverage Subsidies Delayed

- IRS Guidance on Delay of Employer Mandate Penalties and Reporting Requirements

- Employer Reporting of Health Plan Coverage – Code Section 6055 and 6056

- Reporting Requirements for Employers and Health Plans

- Final Rule on Individual Mandate Exemptions and Minimum Essential Coverage

- The Hardship Exemption from the Individual Mandate

- IRS Issues Proposed Rules on Large Employer Reporting Requirements

- Metal Levels for Qualified Health Plans

- Communication Impediments: Are You a 'Cognitive Miser'?

- Networking for Intellectual Capital

- Release of 2012 Advice Memo Pulls Together Principles Applied by the NLRB in Evaluating Employer Social Medial Policies

- Talking About Health Care Insurance

- Email Etiquette

- Culture: Here’s Why It Matters Now More Than Ever Before

- Employee Must-Have Benefits: Revamping the Old, Adding the New

- Employee Care: Wellness and Wellbeing

- Environmental and Sustainability Benefits For Workers

- The Care Factor: The Key to Worker Engagement, Productivity, and Loyalty

- Rising Healthcare Costs: How to Support Employees

- The Great Reshuffle

- Holistic Policies for Caregivers

- Flex-Work Trends

- How Pulse Surveys Can Improve Benefits

- Employers Offering “100% health plans”

- Lifestyle Support For Workers

- Cater Benefits to a Variety of Demographics

- Why Offer Wearables To Your Workforce?

- Improve Member Engagement with Online Portal Services

- Benefits to Attract Top Talent

- Inflation’s Impact on the Cost of Worker Benefits

- Align Family/Work-Life Balance Benefits With Business Goals

- Survey Workers Before Your Next Renewal

- Ways Employers Can Inflation-Proof Workforce Benefits

- Benefits That Help Avoid Employee Burnout

- Work Hour Expectations

- Pet Insurance: A Market with Opportunity

- Coming Back from Parental Leave: How Employers Can Support Workers

- Established Work From Home Benefits

- Benefits of Remote Physical Therapy

- Childcare Trends in the Workplace

- Build a Company Culture That Keeps Employees Happy

- Money Management: The Key To Saving For Retirement

- Popular Voluntary Benefits

- Employee Engagement Strategies

- Get Preventive Care Back on Track

- 2022 Trends: Still Working From Home or Back In the Office?

- Telehealth Trends in 2022

- The Future of Mobile Health Clinics

- Employee Assistance Program vs. Behavioral Health Coverage

- Using Debit Cards For Health Spending Accounts

- Productive Workspace at Home

- Popular Post-COVID Benefit: Pet Insurance

- Digital Eyestrain: Improve Productivity With Vision Benefits

- Short-Term Disability Insurance

- HSA-Approved Expenses For Mental Health

- Engagement Strategies For Remote Workers

- The Benefits of Ergonomics

- Managing Mental Health and Well-Being During COVID-19

- The Demise of One-Size-Fits-All Benefit Plans

- Why and How To Support Moms Back At Work

- Benefits To Help Workers Overcome Stress

- Future of Financial Wellness: Employer-Sponsored Savings Programs

- Convert Unused PTO Into Student Loan Benefit

- How To Maximize Vision Benefits For All Workers

- Prescription Drugs: Brand Name vs. Generic Coverage

- Long Term Care Hybrid Policies: Energizing the Life Insurance Market

- Retiree Medical Plans: What’s Happened to Lifetime Benefits?

- Birth of a New Trend: Commonly Covered Fertility Benefits

- Non-Physical Wellness Benefits: Mental and Financial

- Healthcare Employee Rewards Programs

- Volunteer PTO

- Janus vs AFSCME: Impact On Union-Sponsored Benefits

- Janus vs AFSCME: Impact On Union-Sponsored Benefits

- The True Value of Voluntary Benefits

- Long Term Disability: Big Value, Little Appreciation

- LTD vs. LTC Insurance

- Natural Disaster Leave

- The Underappreciated Cancer Benefit

- Putting Life Back Into Life Insurance

- Welcome Back: How to Support Workers Returning From Disability Leave

- 3 Ways Life Insurance Excels as a Benefit

- Dental Medical Bills

- Pros and Cons of Telemedicine

- Medicare Advantage on the Rise

- Long Term Care Insurance

- How Technology Can Simplify Healthcare Benefits

- The Case For Innovative Benefits

- Customized Benefits

- How Education Benefits Help Reduce Turnover

- Uber Health

- ERISA Disability Rule Update

- Medicare Advantage Update

- Update on Cadillac Tax

- How Group Critical Illness and Accident Plans Supplement Medical Benefits

- Understanding Health Savings Accounts

- Four Benefit Trends in 2018

- How to Engage Employees in Wellness

- Can Your Technology Platform Accommodate Your Benefit Package?

- How to Enhance Your Benefits Communication Efforts

- Most Popular Employee Benefits

- Should You Still Offer Health Insurance as a Benefit?

- How To Attract Top Talent

- Expensive Benefit Plan Penalties to Avoid

- Conditions That Drive Up Employer Healthcare Costs

- Trends in Company Culture

- Changes in Benefits Offerings

- Repeal and Replacement Prospects for Obamacare

- Recent Developments in Wellness Incentive Programs

- Imputed Income

- Reverse Discrimination in Employer Plans

- The Advantage of Mental Health Benefits

- Healthcare Cost Trend

- Saving For Healthcare Expenses

- Telehealth: Redesigning the Patient Experience

- Vision Exams and Insurance Benefits

- Family Medical Leave Act

- Healthcare Reform Updates

- Disability Insurance

- How to Determine Life Insurance Needs

- Pros and Cons of Bundled Benefits

- Value Based Plan Design

- The Alphabet Soup of Medical Plans

- Medicare

- Retiree Medical Accounts

- Cadillac Tax: Implications and Unknowns

- The Facts About Medical Tourism

- The Buy-Up Solution to Curtailing Benefits

- What You Should Know About Prescription Drugs

- HDHP + HSA: A Versatile Savings Combination

- For Your Benefit: HRA, HCFSA and HSA Plans

- OSHA Proposes Rule Requiring Electronic Submission of Injury and Illness Reports

- Dental Insurance: What You Need to Know

- Voluntary Benefits: Adoption Assistance

- What Is Telemedicine?

- Final Rule Implementing Mental Health Parity Requirements

- Senate Passes Gay Rights Legislation

- IRS Clarifies Transition Relief for Cafeteria Plan Elections

- Changes to “Use-or-lose” Rule for Health Flexible Spending Accounts (FSAs)

- EEOC Settles First Genetic Discrimination Lawsuit

- Supreme Court Strikes Down DOMA, Clears Way for Same-Sex Marriage in California

- Supreme Court Limits Employment Discrimination and Retaliation Claims

- Supreme Court Ruling on DOMA – What It Means for Employers

- The Subjectivity of Employee Benefits

- Model HIPAA Privacy Notices Released

- IRS Procedures to Correct Overpayments on Taxes for Same-sex Spouse Benefits

- Limits on Out-of-Pocket Maximums: Full Compliance Delayed for Some Health Plans

- IRS to Recognize All Legal Same-sex Marriages for Federal Tax Purposes

- Guidance Released on Same-sex Marriage Under ERISA

- Work Is Not a Noun; It's a Verb

- Coping With Flu Season: 3 Tips to Encourage Sick Workers to Stay Home

- Attract and Retain: What Does “Gen Next” Want?

- Retention and Attraction: Cherish or Perish

- The Resilient and the Restless

- How to Attract and Retain Quality Workers in an Environment Poised for Turnover

- A Checklist for Hiring the Very Best Talent

- Employees Make It Clear: Here's What They Need to Really Be Engaged